Bitcoin Is Reacting to Global Financial Conditions

The macro shortage of dollars is hammering hard assets — and Bitcoin is the cleanest signal

Look. What just happened to Bitcoin and gold this month was not a crypto winter. It was not some random risk-off vibe shift. It was the mechanical, predictable output of a global dollar shortage doing exactly what it always does when it shows up. Read that again, because it matters: this wasn’t Bitcoin failing. This was Bitcoin measuring something true.

Here’s the architecture. The world runs on an offshore dollar credit machine that dwarfs anything the Fed directly controls — trillions in dollar-denominated debt, carry trades, and funding lines sitting outside the United States, invisible until they aren’t. When that machine tightens, leveraged players do not ask politely for more runway. They sell what’s liquid to raise dollars. Fast. That is what June was.

You can see the fingerprints everywhere. Gold just posted its worst quarterly decline since April 2013 — down roughly 24% from its late-January all-time high near $5,589 an ounce, breaking below $4,000 for the first time since November as a resurgent dollar and a market that flipped from pricing rate cuts to pricing rate hikes did the damage. Bitcoin fell in the same window for the same root cause. Both assets are pristine, bearer collateral. Gold is the credit-market asset — it thrives when credit expands and gets crushed when liquidity drains. Bitcoin is the purest read on banking-system liquidity itself, because it has no yield to hide behind and no central bank that can print more of it to paper over the stress.

This is the system’s fatal flaw showing its face. There is no shortage of dollar printing presses. There is a shortage of trustworthy distribution. When confidence cracks or policy tightens, the dollars that already exist get hoarded onshore, and everyone else — sovereigns, corporates, leveraged funds — has to sell whatever they can to get their hands on them. That’s not a rejection of Bitcoin. That’s the market forcing the plumbing to reveal how brittle it’s become.

The yen is the textbook right now. It just hit its weakest level against the dollar in nearly forty years — north of 162 yen per dollar as of June 30 — even after the Bank of Japan hiked rates to 1% on June 16 and Japan spent roughly $72.5 billion defending the currency between April and May. That is the fourth consecutive quarterly loss for the yen, the longest losing streak in four years. Cheap yen funded trades all over the world for over a decade. Every time this year that funding trade got squeezed — February, again in May — Bitcoin took a hit within hours, not because of anything happening in crypto, but because deleveraging doesn’t check your asset class before it sells you.

Here’s the thing about where the money actually went. It didn’t vanish. Since April, U.S. gold and Bitcoin ETFs have bled roughly $12 billion in cumulative outflows — while U.S. semiconductor ETFs pulled in about $20 billion over the same stretch. That’s not the market rejecting hard money. That’s capital rotating into a narrow slice of AI infrastructure trades while pristine collateral gets sold to fund the move and cover margin elsewhere. In a real liquidity squeeze, the most transparent, most liquid risk asset gets hit first. That’s Bitcoin doing exactly what it was designed to do — pricing the true state of global financial conditions without a central bank standing behind it to smooth the read.

The people who understand monetary reality are not confused by any of this. They’re using it. Strategy just built a $1.25 billion Bitcoin monetization framework — its first real optionality to sell since 2022 — not because Michael Saylor lost conviction, but because a mature treasury company manages liquidity through cycles instead of pretending cycles don’t exist. That’s discipline, not doubt. Meanwhile the fixed supply of 21 million coins does not care about offshore funding gaps or carry trade reversals. It sits there. Verifiable. Portable. Impossible to dilute. While everything else in the world reprices around a scramble for dollars that Bitcoin was built specifically to make obsolete.

Bitcoin Market Nearing a Bottom

Here’s the thing. Bitcoin is trading near $58,000–$59,000 as July begins — call it $60,000 if you’re rounding generously, but the honest number sits just under it. That’s a drawdown of roughly 53% from the cycle high of $126,198.07 set in October 2025. Nine months into this bear phase now. Nine months of chop, tight liquidity, and sentiment pinned in extreme fear.

Look at the structure and it reads like a late-stage bear that’s already flushed its leverage. Immediate support sits in the mid-to-high $50Ks — a zone where prior cycle lows and options hedging interest cluster, and where Peter Schiff has publicly warned that a failure to hold risks a slide toward $50,000 outright. A sustained break below that opens the door to deeper structural support in the low-to-mid $50Ks. On the upside, the first real resistance cluster lives in the low-to-mid $60Ks, with the mid-to-high $60Ks as the broader ceiling. Reclaim and hold that zone and this stops being damage control and starts being base-building. Beyond that, the low-to-mid $70Ks is the next decision point, where trapped supply from earlier in the cycle could resurface as sellers.

June’s ETF flows were not just weak. They were historic — roughly $4.5 billion in net outflows for the month, the worst on record for the spot Bitcoin ETF complex since it launched, capping a nine-day outflow streak into month-end. Read that again: this is the largest monthly redemption these products have ever seen. And yet the cumulative institutional bid across the full cycle remains real. Corporate treasury accumulation continued through June — Strategy added roughly 3,600 more BTC across three separate purchases, pushing its stack to 847,363 coins. One thing worth being straight about: Strategy also authorized a $1.25 billion Bitcoin monetization framework on June 29, its first standing capacity to sell since 2022. That’s not panic. That’s a mature treasury managing liquidity through a brutal stretch instead of pretending brutal stretches don’t happen. But it does mean the “accumulation without volatility” era has a new wrinkle, and it’s worth watching rather than waving away.

Sentiment has stayed in extreme fear for an extended run. That is the exact condition under which every prior cycle low has formed. Exhausted leverage, institutional buyers stepping in on weakness, and a macro backdrop that’s still a global system short trustworthy dollar distribution — all three point the same direction. The forced-selling phase looks like it’s mostly behind us. What’s left is the chop and the base-building that every prior bear market has run through before the next liquidity cycle turns.

The macro dollar shortage created this moment. Fixed supply and the institutional infrastructure now in place are what turn this moment into the foundation for whatever comes next. Price is just the mechanism that moves ownership from the hands that can’t hold through the squeeze into the hands that can.

Bitcoin is nearing the end of the its Bear Cycle in both time & price

Institutional Rails Are Accelerating Precisely Because of the Dollar Shortage

While price reacts to the liquidity squeeze, the actual monetary network is being wired deeper into the financial system. Here’s the thing — banks, fintechs, and payment companies are not building these rails because markets are calm. They are building them because the legacy collateral and settlement systems keep proving, cycle after cycle, that they cannot handle a dollar shortage without forcing fire sales of real assets.

Lightning infrastructure now supports instant, low-cost settlement across borders without requiring correspondent banking relationships that can freeze or delay dollars exactly when you need them most. Institutional custody has matured to the point where regulated entities hold Bitcoin as collateral for lending and treasury operations without the rehypothecation risk baked into traditional systems. And Bitcoin-backed lending is no longer a niche experiment — Silicon Valley Bank put a number on it this year: the Bitcoin-backed lending market has grown to roughly $67 billion. Ledn closed the first investment-grade-rated Bitcoin-backed bond in February, a $188 million deal rated BBB- by S&P Global and oversubscribed two times over. Strike secured a $2.1 billion credit facility from Tether and now offers loans as low as 7.5% APR on size. This is not a fringe product anymore. It’s plugging directly into the same asset-backed securities machinery that already funds mortgages and car loans.

Look at what just happened in housing. Better and Coinbase funded the first Fannie Mae-backed conventional mortgage collateralized by Bitcoin in June, with nationwide rollout planned for this summer. A borrower pledges Bitcoin, gets a loan against it, and never triggers a taxable sale or gives up the upside. That’s not a press release about the future. That is already closed.

None of this is happening in spite of the macro pressure. It is happening because of it. When offshore dollar funding tightens, the institutions that must still move value and post collateral look for the one asset that is globally portable, instantly verifiable, and impossible to double-pledge. Bitcoin is that asset. The same dollar shortage forcing weak hands to sell is simultaneously proving why the hardest, most transparent form of collateral is becoming indispensable.

Corporate treasuries made this calculation a long time ago. Strategy alone holds more than 4% of the total Bitcoin supply on a single balance sheet — 847,363 coins — and it isn’t close to alone anymore. More than 170 publicly traded companies now carry Bitcoin as a treasury reserve asset, collectively holding well over a million coins. Accounting changes removed the previous friction. Macro reality removed any remaining doubt. When cash balances lose purchasing power and traditional reserves correlate with the same liquidity squeezes that are hammering everyone else, the asset with absolute scarcity and no counterparty stops being a bet. It becomes the obvious upgrade.

Altcoins Continue to Bleed While a Few Build in the Dark

Most of the altcoin market remains in liquidation mode. Capital is still flowing out of the sector as a whole, both in dollar terms and versus Bitcoin. The majority of projects continue to demonstrate exactly what they always were: speculative vehicles with no durable demand and no path to surviving a prolonged liquidity contraction. The casino phase is ending the only way it can — through attrition.

A small handful of projects are showing different behavior. Solana continues to post high on-chain activity and daily active users even while its token price remains depressed more than 60 percent from cycle highs. The network is actually being used for payments and decentralized applications at scale. Ethereum’s layer-2 stack and real-world asset tokenization pipeline are progressing, albeit slowly, with institutions still exploring the rails even in a risk-off environment. XRP has seen meaningful ETF inflows relative to its size, suggesting some institutional interest in its cross-border use case. Hyperliquid has maintained impressive trading volumes on its decentralized perpetuals exchange despite token price weakness.

These are the survivors taking shape. They are not immune to the broader liquidity squeeze, but they are demonstrating real usage and product traction while everything else dies. That distinction matters for the next cycle. It does not change the current stance: until Bitcoin itself stabilizes and global liquidity conditions improve in a sustained way, fresh capital deployment into altcoins remains on hold. Bitcoin first. Dry powder second. Altcoins only after they have earned their place through actual adoption rather than narrative.

The macro shortage of dollars is not a Bitcoin problem. It is the predictable consequence of a financial system built on abundant but poorly distributed fiat credit. Bitcoin’s price is reacting exactly as its design intends — measuring the stress in real time and transferring ownership to those with the conviction to hold the hardest money through the squeeze. The institutions building the rails and accumulating the supply are not waiting for permission or perfect conditions. They are acting while the crowd is still focused on the candles.

Claude AI Bitcoin Market Analysis

Where We Stand

Bitcoin enters July trading near $58,700, a drawdown of roughly 53% from the all-time high of $126,198.07 set on October 6, 2025. June closed red — down close to 19–20%, the worst monthly performance since June 2022 — which puts May and June together as a fresh two-month losing streak. That streak followed two green months, March and April, so this is not a continuation of any extended multi-month skid. It is a new leg down, and it is the deepest one this cycle has produced outside the initial correction off the peak.

Read that number again. Fifty-three percent below the high. That sits meaningfully worse than the 42% drawdown this blog was tracking back in early June, and it confirms what the price action was already signaling: the floor that was supposed to hold in the mid-$60Ks did not hold, and the next one down didn’t either.

Sentiment Picture

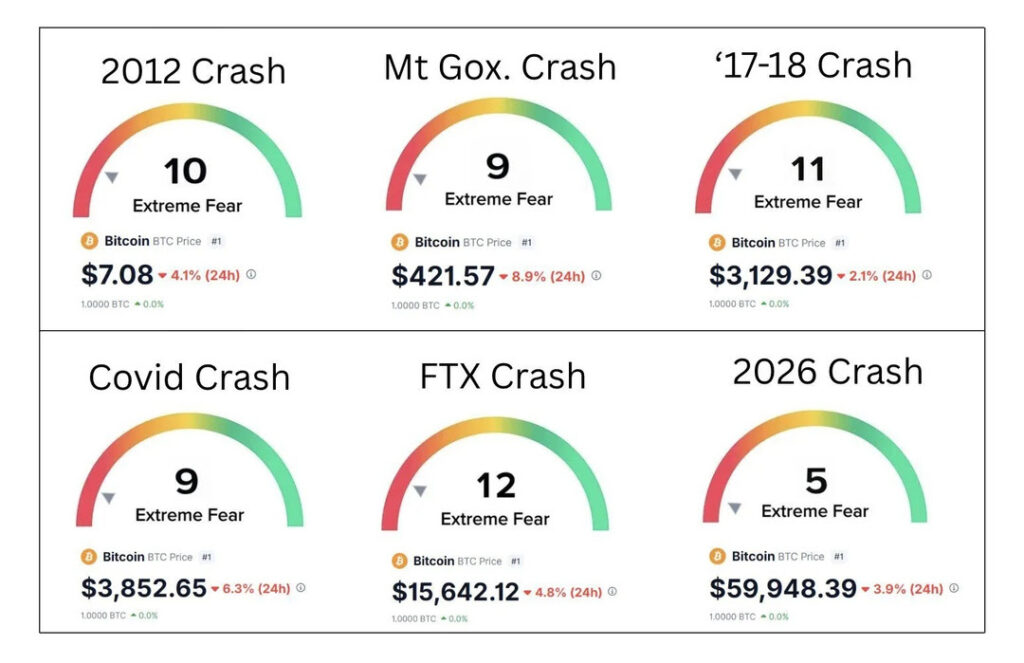

The classic Fear & Greed Index sits at 11 — Extreme Fear — as of today, down from 15 the prior session. Worth flagging plainly: a separate composite index (CFGI) reads 44, Neutral, on a different methodology that weights derivatives positioning more heavily. The two disagree because one is measuring crowd emotion and the other is measuring options structure, and right now those two things are telling different stories. We’re defaulting to the classic index here because it’s the one this blog has tracked historically, and because it lines up with everything else in the picture — nine-day ETF outflow streaks, a record monthly redemption, and a token BTC sale from the largest corporate holder in the world don’t happen in a Neutral market.

This is not a one-week wobble. Sentiment has been pinned in Fear-to-Extreme-Fear territory for an extended run stretching back through the spring, with only brief, short-lived visits to neutral. Historically, this is exactly the emotional terrain cycle lows get built in. Not when the timeline is celebrating. When it’s exhausted.

The Critical Divergence

June is where retail and institutional behavior split hardest, and the split cuts two directions at once — worth being honest about both.

On one side: U.S. spot Bitcoin ETFs posted their worst month on record, roughly $4.5 billion in net outflows, a nine-day outflow streak running straight into month-end. That is not a soft patch. That is the largest monthly redemption these products have ever seen since they launched.

On the other side, corporate treasuries kept buying. Strategy added roughly 3,600 BTC across three separate purchases in June, pushing its total holdings to 847,363 coins — more than 4% of the entire supply that will ever exist — at an average cost basis of $75,651 per coin. Every one of those June purchases was made at a loss to average cost, and they bought anyway.

Here’s the wrinkle that has to be said plainly: on June 1, Strategy sold Bitcoin for the first time since 2022 — a token 32 coins — and on June 29 the board authorized a $1.25 billion BTC Monetization Program, giving itself standing capacity to sell up to roughly 2.5% of its stack. That is not the same company that spent three straight years only ever adding. It is a company that just built itself an exit valve. The honest read: this is disciplined treasury management from a firm whose stock premium to its Bitcoin holdings has compressed, not a change in long-term conviction — Strategy still net-added BTC in June, at a loss, while building that capacity. But calling it “accumulation without volatility” would no longer be accurate, and that distinction matters more this month than it did last.

Technical Structure

Bitcoin is trading near $58,700 against an all-time high of $126,198.07 — a 53% drawdown, deeper than the correction that ran through most of this cycle, though still short of the 77% peak-to-trough collapse that marked the 2021–2022 cycle low.

The 52-week range runs from $57,950 at this week’s low to $126,198.07 at the October peak. Bitcoin is trading at roughly 47% of its 52-week high.

The daily RSI sits in the high-20s to high-30s depending on the data source — oversold to approaching oversold, consistent with conditions that have historically preceded relief rallies, though oversold readings can persist through a genuine trend rather than resolving immediately. The 200-day moving average sits near $61,000 and has been falling since early June, now representing the first meaningful resistance overhead. The 50-day moving average sits just above current price near $59,600, acting as immediate resistance.

Key levels heading into July: immediate support sits at $58,000, with deeper structural support in the mid-to-high $50Ks if that fails. Immediate resistance sits at $61,000–$61,500 — reclaiming and holding that zone would be the first real signal of base-building rather than continued bleeding. Beyond that, $65,600 marks the next major overhead level tied to the 50-month EMA, and a decisive move above it would be the first legitimate technical sign the correction phase is ending.

Macro Overlay

The dollar shortage thesis that’s carried this entire edition of the blog has hard data behind it this month. Gold just posted its worst quarterly decline since April 2013, down roughly 24% from its late-January all-time high near $5,589, driven by a market that flipped from pricing Fed rate cuts to pricing rate hikes. The U.S. Dollar Index sits at its strongest level in over a year. The Fed has held its benchmark rate at 3.50–3.75% through the spring, and markets are no longer pricing the easing cycle they expected at the start of 2026.

The yen carry trade is the clearest transmission mechanism. The yen just touched its weakest level against the dollar in nearly forty years — north of 162 per dollar as of June 30 — even after the Bank of Japan hiked to 1% on June 16. Every time this year that trade got squeezed hard — February, then again in May — Bitcoin took a hit within hours, independent of anything happening in crypto specifically.

And capital rotation is showing up in the flow data directly: since April, U.S. gold and Bitcoin ETFs have posted roughly $12 billion in cumulative outflows, while U.S. semiconductor ETFs pulled in roughly $20 billion over the same window. That’s not a rejection of hard money. That’s capital concentrating into a narrow AI trade while pristine collateral gets sold to fund the move.

Monthly Outlook: Three Scenarios

Bullish Case — Probability: 20%. Bitcoin reclaims $61,000–$61,500 in the first half of July and holds it, converting resistance into support. ETF outflows meaningfully slow or reverse, sentiment lifts out of Extreme Fear toward neutral, and price pushes toward the $65,600 level. A clean break above that opens a path toward $70,000. This requires both a technical reclaim and a genuine flow reversal — neither has happened yet.

Neutral Case — Probability: 50%. Bitcoin chops between $57,000 and $62,000 through most of July, absorbing the aftershock of June’s record ETF outflows without a decisive break in either direction. Sentiment stays in Fear but doesn’t deteriorate meaningfully further. Corporate treasuries keep buying on weakness. This is the scenario where the market builds a base the hard way — sideways, ugly, unglamorous — and patient accumulators are rewarded relative to anyone trying to trade the chop.

Bearish Case — Probability: 30%. The $58,000 support fails to hold on a sustained basis, opening the door toward the mid-to-high $50Ks and, if that fails too, the low $50Ks — a level Peter Schiff and others have explicitly flagged as the line that separates orderly correction from capitulation. This scenario would likely require either a fresh yen-carry shock, a deeper equity/AI-trade unwind, or another leg of ETF selling beyond June’s record pace. Even here, a full repeat of the 2021–2022 cycle’s 77% drawdown would put a floor near $29,000 — a level that, given current institutional infrastructure and treasury dynamics, no credible analyst is currently treating as a realistic target.

The Number That Matters Most

847,363. That’s how many Bitcoin Strategy now holds — more than 4% of the total supply that will ever exist, on one balance sheet, acquired at an average cost of $75,651 per coin. Every coin bought in June was bought underwater relative to that average. They bought anyway, even while building themselves a $1.25 billion escape hatch on June 29 in case they ever need one.

That’s not contradiction. That’s what a company run by someone who has done the math looks like when markets get uncomfortable: keep buying the asset you believe in structurally, while giving yourself optionality on the balance sheet you actually have to manage day to day. The supply keeps concentrating. The float everyone else has to compete for keeps shrinking. Fixed supply, growing institutional claim on that supply — that math only resolves one way over time, even when the path there looks like June did.

Summary and Strategy

Here it is in Saylor’s language: Bitcoin at $58,700 against an ATH of $126,198.07 and a corporate treasury cost basis of $75,651 per coin is not a broken thesis. It is a 53% discount on the scarcest asset in human history, arriving during the most acute dollar-distribution stress this cycle has produced. Every purchase made in this zone — corporate or individual — is a purchase made at a price that a decade of monetary history says gets remembered as generational, not foolish.

Here it is in Mallers’ language: Look. The fiat plumbing is cracking in front of you. Gold just had its worst quarter since 2013. The yen just hit a forty-year low. The Fed is stuck between inflation it can’t fully suppress and a debt load it can’t afford to defend with high rates forever. Bitcoin ETFs just posted their worst month ever — and the largest Bitcoin holder on Earth bought more anyway, at a loss, while quietly building itself room to breathe. That’s not panic. That’s what conviction looks like when it has to survive contact with a real market instead of a chart.

The window is open. It always feels like it’s closing hardest right before it doesn’t.

Final Thoughts

Look — step back for a second and take in the whole board, because no single section of this edition tells the real story on its own.

The macro backdrop is a global dollar shortage doing exactly what it always does when offshore credit tightens: forcing the sale of anything liquid enough to raise cash fast, which is why Bitcoin and gold got hit together this month even as a narrow slice of AI-adjacent stocks kept climbing. That is not Bitcoin failing. That is Bitcoin measuring the truth of a financial system that keeps proving it cannot distribute dollars without breaking something. Price is sitting near $58,700, down 53% from the October all-time high, closing out a fresh two-month red streak after June posted its worst month since 2022. The floor that was supposed to hold in the mid-$60Ks gave way, and the one below it gave way too. That is the honest, unflattering truth of where this correction sits right now, and pretending otherwise would insult everyone reading this.

And yet — here is the part that matters more. While price bled, the actual monetary network kept getting built deeper into the financial system. Lightning settlement, matured institutional custody, a Bitcoin-backed lending market that just crossed $67 billion, an investment-grade Bitcoin-backed bond rated by S&P, and the first Fannie Mae-backed mortgage in American history collateralized by Bitcoin — all of that happened during the same stretch the headlines were calling this a crypto winter. More than 170 public companies now hold Bitcoin as a treasury reserve asset, collectively controlling well over a million coins, and Strategy alone sits on more than 4% of the entire supply that will ever exist. They bought more of it in June, underwater, while building themselves room to breathe with a new monetization framework. That is not doubt. That is what discipline looks like when conviction has to survive contact with a real market.

The altcoin market, meanwhile, is doing exactly what a real bear market is supposed to do — separating the tokens with actual usage from the ones that were only ever a story. Solana’s price sits near multi-year lows while its network just posted an all-time-high quarter of transactions. XRP just logged eight straight weeks of ETF inflows while its price fell, which is what allocators do when they’re building a position instead of chasing one. Hyperliquid just took a record share of global derivatives volume during the same month the broader market lost a quarter of its value. Everything else is still bleeding out, and it should be. That is the casino closing, not the industry dying.

Sentiment is sitting in Extreme Fear, and that is precisely the emotional weather every prior Bitcoin cycle low has been built in. Not euphoria. Exhaustion. The ETF wrapper just posted its worst month ever — $4.5 billion out the door — while the world’s largest corporate holder of Bitcoin kept adding coins at a loss to its own average cost. Retail is scared. Institutions are still buying. That divergence has been the signal every single cycle, and this one is no different.

Here’s the thing you have to hold onto through a month like this one: none of the forces that make Bitcoin what it is have changed. Twenty-one million coins. No central bank behind it that can print more when the pressure gets uncomfortable. No counterparty that can fail and take your collateral down with it. The dollar shortage that’s hammering every asset on the planet right now is the exact condition Bitcoin was engineered to outlast. It doesn’t need the squeeze to end to remain scarce. It just needs to still exist when the squeeze does end — and every signal in this edition says it’s not going anywhere.

The window is open right now precisely because it feels like it’s slamming shut. It has felt that way at every real bottom this asset has ever built, and it will feel that way again the next time. It never actually closes. It just gets more expensive, quietly, for everyone who waited for the fear to pass before they acted. Stack accordingly.

All information provided is for educational purposes only. It is essential to conduct your own research before making any financial decisions. This is not intended as financial advice.

Links & Tutorials

Bitcoin Education Resources

Hope.com – Learn more about Bitcoin and how to use BTC to protect your wealth.

The Bitcoin Standard – Book by Saifedean Ammous – a must-read!

Crypto 101 – A beginner handbook to cryptocurrency

The Bitcoin Way – Go bankless! Bitcoin education and services to help you custody your Bitcoin safely and securely.

Swan Bitcoin – Bitcoin exchange, IRAs and institutional-grade custody solutions

River Financial – Bitcoin exchange and institutional-grade custody solutions

God Bless Bitcoin – Full Length Documentary

Zero To Hero Bitcoiner – Tutorials from BTC Sessions

Freedom People Resources

People Pay – Accept Bitcoin payments for your business

Chainrecorder – Prove ownership immutably by recording your documents on the Bitcoin blockchain

Cracking the Code Educated Tax Return – Legally avoid income and capital gains taxes.

U.S. Regulated Exchanges (Fiat Onramps)

Coinbase – Using Coinbase Advance Video

Kraken – Using Kraken Pro Video

KYC Credentials Outside the U.S.

Palau ID – Foreign residence to pass KYC on foreign exchanges.

KYC Exchanges that Accept Palau ID (Must Use VPN – Costa Rica, Columbia, Mexico, Panama)

No KYC Exchanges (Must Use VPN – Costa Rica, Columbia, Mexico, Panama)

DEXs (Decentralized Exchanges) – Best Wallet To Use

Jupiter – Video Solana Ecosystem – Phantom Wallet

Whales Market – Solana OTC Trade Desk – Phantom Wallet

Thorswap – Swap native assets cross-chain (BTC for ETH etc..) and a very unique decentralized Bitcoin lending platform. Works best with the XDefi Browser Wallet.

Decentralized Bitcoin lending platform. Thorswap Overview Video Loans On Thorswap Video

Osmosis – Cosmos Ecosystem – Rabby, Metamask

Spooky Swap -Fantom – Rabby, Metamask

Trader Joe – Avalanche Ecosystem – Rabby, Metamask

Crypto Market and Portfolio Tracking

CoinGecko for portfolio tracking and up-to-date prices

CoinMarketCap – Crypto Prices

Banter Bubbles – Crypto Prices – Social Sentiment

Trading View – Chart all Markets and trading pairs Tradingview Tutorial Video

Storage – Not your keys, Not your crypto!

Cold Storage Wallets (Secure Long-Term Storage of Your Crypto)

Nunchuk – Multi Signature Wallet and Inheritance Service

Casa Custody Solutions – Multi Sig Storage and Inheritance

Cold Card (Bitcoin Only) – Video

Hot Wallets (Lower Security – interact with DAPPS and Smart Contracts)

Bull Bitcoin Wallet – Video Bitcoin Wallet with Privacy features

XDefi Browser Wallet – Video1 Video 2

Aqua Wallet – Video – Self Custody, Lightning and Liquid Network Bitcoin & USDT

Warning-If you have a wallet and an NFT has been sent to your wallet that you did not mint or purchase.. NEVER click on it. Many have malicious code that can drain your wallet! – BE CAREFUL

Stay Free!

Kury

You must be logged in to post a comment.